Pre-colonial

The citizens of the Indus Valley civilisation (based around the river Indus in modern day Pakistan and Northern and Western India), a permanent and predominantly urban settlement that flourished between 2800 BC and 1800 BC, practised agriculture, domesticated animals, used uniform weights and measures, made tools and weapons, and traded with other cities. Evidence of well planned streets, a drainage system and water supply reveals their knowledge of urban planning, which included the world's first urban sanitation systems and the existence of a form of municipal government.

The 1872 census revealed that 99.3% of the population of the region constituting present-day India resided in villages, whose economies were largely isolated and self-sustaining, with agriculture the predominant occupation. This satisfied the food requirements of the village and provided raw materials for hand-based industries, such as textiles, food processing and crafts. Although many kingdoms and rulers issued coins, barter was prevalent. Villages paid a portion of their agricultural produce as revenue to the rulers, while its craftsmen received a part of the crops at harvest time for their services.

Religion, especially Hinduism, and the caste and the joint family systems, played an influential role in shaping economic activities. The caste system functioned much like medieval European guilds, ensuring the division of labour, providing for the training of apprentices and, in some cases, allowing manufacturers to achieve narrow specialization. For instance, in certain regions, producing each variety of cloth was the speciality of a particular sub-caste.

Textiles such as muslin, Calicos, shawls, and agricultural products such as pepper, cinnamon, opium and indigo were exported to Europe, the Middle East and South East Asia in return for gold and silver.

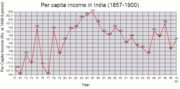

Assessment of India's pre-colonial economy is mostly qualitative, owing to the lack of quantitative information. One estimate puts the revenue of Akbar's Mughal Empire in 1600 at £17.5 million, in contrast with the total revenue of Great Britain in 1800, which totalled £16 million. India, by the time of the arrival of the British, was a largely traditional agrarian economy with a dominant subsistence sector dependent on primitive technology. It existed alongside a competitively developed network of commerce, manufacturing and credit. After the fall of the Mughals, India was administered by Maratha Empire. The maratha empire's budget in 1740s, at its peak, was Rs. 100 million. After the loss at Panipat, the maratha empire disintegrated into confederate states of Gwalior, Baroda, Indore, Jhansi, Nagpur, Pune and Kolhapur. Gwalior state had a budget of Rs. 30M. However, at this time, British East India company entered the Indian political theatre. Until, 1857, when India was firmly under the British crown, the country remained in a state of political instability due to internecine wars and conflicts.

Colonial

Colonial rule brought a major change in the taxation environment from revenue taxes to property taxes resulting in mass impoverishment and destitution of the great majority of farmers. It also created an institutional environment that, on paper, guaranteed property rights among the colonizers, encouraged free trade, and created a single currency with fixed exchange rates, standardized weights and measures, capital markets, a well developed system of railways and telegraphs, a civil service that aimed to be free from political interference, and a common-law, adversarial legal system. India's colonisation by the British coincided with major changes in the world economy—industrialisation, and significant growth in production and trade. However, at the end of colonial rule, India inherited an economy that was one of the poorest in the developing world, with industrial development stalled, agriculture unable to feed a rapidly growing population, one of the world's lowest life expectancies, and low rates of literacy.

An estimate by Cambridge University historian Angus Maddison reveals that India's share of the world income fell from 22.6% in 1700, comparable to Europe's share of 23.3%, to a low of 3.8% in 1952. While Indian leaders during the Independence struggle, and left-nationalist economic historians have blamed colonial rule for the dismal state of India's economy in its aftermath, a broader macroeconomic view of India during this period reveals that there were sectors of growth and decline, resulting from changes brought about by colonialism and a world that was moving towards industrialisation and economic integration.While the exact sectors of growth and decline is of questionable importance, the overall effect of the changes brought about by colonialism, and India's degree of industrialisation and economic integration of India under the British rule on India's economy can be assessed from the kind of economy India inherited after the end of the colonial rule in India.

Independence to 1991

Indian economic policy after independence was influenced by the colonial experience (which was seen by Indian leaders as exploitative in nature) and by those leaders' exposure to Fabian socialism. Policy tended towards protectionism, with a strong emphasis on import substitution, industrialization, state intervention in labour and financial markets, a large public sector, business regulation, and central planning Jawaharlal Nehru, the first prime minister, along with the statistician Prasanta Chandra Mahalanobis, carried on by Indira Gandhi formulated and oversaw economic policy. They expected favourable outcomes from this strategy, because it involved both public and private sectors and was based on direct and indirect state intervention, rather than the more extreme Soviet-style central command system. The policy of concentrating simultaneously on capital- and technology-intensive heavy industry and subsidising manual, low-skill cottage industries was criticized by economist Milton Friedman, who thought it would waste capital and labour, and retard the development of small manufacturers.

India's low average growth rate from 1947–80 was derisively referred to as the Hindu rate of growth, because of the unfavourable comparison with growth rates in other Asian countries, especially the "East Asian Tigers".

After 1991

In the late 80s, the government led by Rajiv Gandhi eased restrictions on capacity expansion for incumbents, removed price controls and reduced corporate taxes. While this increased the rate of growth, it also led to high fiscal deficits and a worsening current account. The collapse of the Soviet Union, which was India's major trading partner, and the first Gulf War, which caused a spike in oil prices, caused a major balance-of-payments crisis for India, which found itself facing the prospect of defaulting on its loans. In response, Prime Minister Narasimha Rao along with his finance minister Manmohan Singh initiated the economic liberalisation of 1991. The reforms did away with the Licence Raj (investment, industrial and import licensing) and ended many public monopolies, allowing automatic approval of foreign direct investment in many sectors. Since then, the overall direction of liberalisation has remained the same, irrespective of the ruling party, although no party has tried to take on powerful lobbies such as the trade unions and farmers, or contentious issues such as reforming labour laws and reducing agricultural subsidies.

Since 1990 India has emerged as one of the wealthiest economies in the developing world; during this period, the economy has grown constantly, but with a few major setbacks. This has been accompanied by increases in life expectancy, literacy rates and food security.

While the credit rating of India was hit by its nuclear tests in 1998, it has been raised to investment level in 2007 by S&P and Moody's. In 2003, Goldman Sachs predicted that India's GDP in current prices will overtake France and Italy by 2020, Germany, UK and Russia by 2025 and Japan by 2035. By 2035, it was projected to be the third largest economy of the world, behind US and China.

No comments:

Post a Comment